{kind=link}

Before I started this website, I worked in the municipal bond business. Everyone in that world knows New Jersey’s finances are a basket case. However, no one is talking about right now is how badly the the latest stock market crash has affected the New Jersey Teachers’ Pension Fund. It speeds up the timeline for Armageddon in New Jersey by years. People are lazy. They look at the latest published reports for their information. However, by simply extrapolating their cash burn rate it is clear that the New Jersey Teachers’ Pension Fund will run out of money. The fund will be totally gone within 10 years. New Jersey will owe billions in payments to retired teachers that it doesn’t have. At that point, I conservatively estimate that New Jersey slashes teacher pensions by 50% and New Jersey raises taxes by about 30%.

New Jersey’s politicians tried to hide the ticking time bomb of pensions for years. Within this decade, they will not be able to contain the explosion. I am profiling the Teachers’ Fund because it will be the first to go into crisis. The fund has the worst funding ratio of the large public pension plans in New Jersey. If you doubt me or think I’m kidding, keep reading below. I have the figures to prove it.

Falling Pension Values and late investment reports

The New Jersey Teachers’ Pension Fund valuation stood at $27.323 billion on June 30, 2014. As of this article’s publication, New Jersey has not published the official report for the fund for the fiscal year ending June 30, 2015. In addition, they have not posted a monthly investment report for the fund since October 2015 (Update: they seem to publish monthly performance reports 2-3 months late). Total New Jersey Teachers’ Pension Fund assets on June 30, 2014 were $81.22 billion. Total fund assets across all public sector pension plans as of October 31, 2015 were $74.03 billion, a 8.85% decrease (Update: They are down to $70.8 billion as of end of March 2016).

The Stock Market Drop and extrapolating the NJ Teachers’ Pension value

If we assume that the fund saw the same drop, that would put its assets at $24.9 billion. Now for the scary part. As anyone who has looked at their online 401k statements knows, the stock market fell the past two and a half months since the last time New Jersey posted their investment returns. If you look at their investment reports, about 50%-70% of the New Jersey Teachers’ Pension Fund assets should reflect the returns of the stock market. Half of that is in US stocks, and the other half is in equity investments that have performed even more poorly than US stocks.

Since New Jersey’s last investment report, the broad US stock market is down more than 10%. Broad International markets are down close to 14%. The fund also holds emerging market stocks and venture capital that might be down more than that. Say 60% of the New Jersey Teachers’ Pension Fund is down 12% and the rest is unchanged. That means the fund itself has lost 7.2% of its value since the latest investment report. That would put my extrapolated pension value down at closer to $23.1 billion.

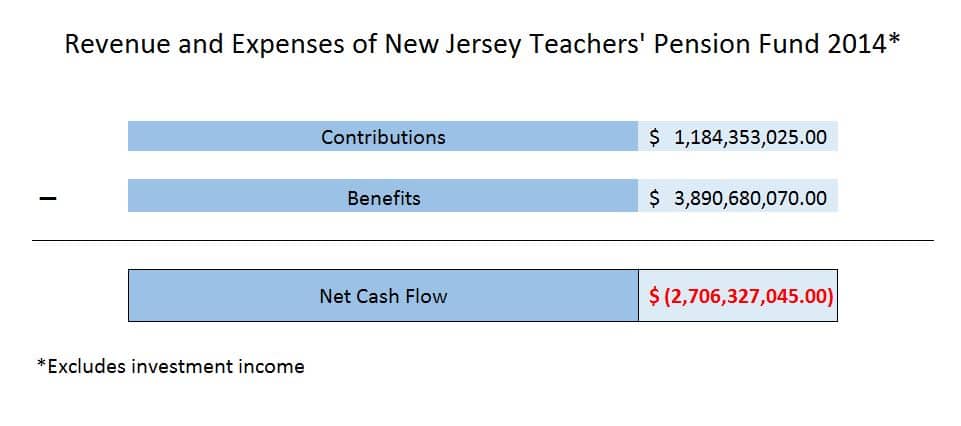

Large Negative Net Cash Flow

That’s the figure I’ll operate off of to prove that the New Jersey Teachers’ Pension Fund is doomed. Take a look at the annual loss the fund was experiencing, before investment income on the pension fund, as of end of the 2014 fiscal year.

Normally, a pension fund could earn the remaining $2.7 billion and the fund would be in balance. However, that can’t happen when a fund is only at $23.1 billion. That would imply an annual return of 11.6% a year. Based on realistic assumptions, I calculate that after accounting for investment income, New Jersey’s Teachers’ Pension Fund is burning through $1.5 billion a year, and that figure is growing.

Christie Has a Ridiculous Investment Return Assumption

A quick primer on rates of return. State politicians come up with a rate of return they hope the New Jersey Teachers’ Pension Fund can get and base their contributions accordingly. Over the past 30 years, a mixed portfolio of stock and bonds has generally been able to achieve 8%. That’s because of falling interest rates and an increase in the Price Earnings multiple for the stock market. In other words, the past 30 years are impossible to repeat mathematically. A high return assumption means you don’t have to contribute as much to the pension. A low pension return assumption means you have to contribute a lot. New Jersey assumes a really high return, and the whole reason is to avoid paying the billions of dollars they would have to if they were being honest.

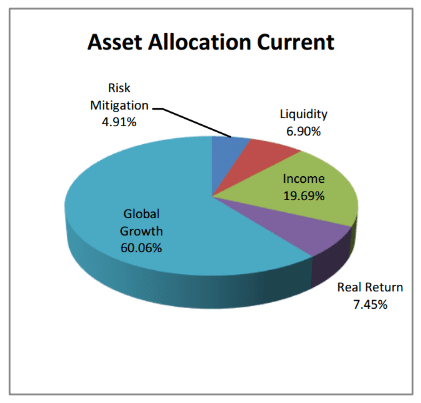

The New Jersey Teachers’ Pension and Annuity Fund’s (TPAF for short) assumed rate of return is 7.9%. Is that a realistic number? Should we expect the pension investment committee capable of achieving this rate? They already reduced the return assumption from 8.25% to its present 7.9%, but they didn’t reduce it enough. In fact, it is absurd to think that the New Jersey Teachers’ Pension Fund can earn that high a rate of return over the next 10 years. To see why, look at their asset allocation. I pulled it directly from New Jersey’s own Treasury Dept website.

Breaking Down What New Jersey Needs to Earn on the stock portion of the Portfolio

I’ll save you from pouring through their monthly Investment reports and tell you what the chart means above. “Global Growth” is mostly publicly traded stocks. “Real Return” is commodities and real estate. “Risk Reduction” is a market neutral hedge fund. “Income” is mostly corporate, US, and international bonds. “Liquidity” is cash and short term Treasury bills. To figure out a realistic return assumption we just need to figure out what we could expect from each of the parts and put them together.

Liquidity is easy. It’s just the same kind of stuff banks buy and give you 0.15% in your checking account with. It’s super short term securities that currently yield almost nothing, so let’s be charitable and assume NJ could earn 0.2% a year from this category. The return from Income can be approximated by looking at the Yield on a broadly diversified mutual fund. I’ll use 2/3 VG Intermediate Term Investment Grade Bond Index Fund and 1/3 Total International Bond Index Fund. Those SEC Yields are listed on Vanguard’s website as 2.82% and 1.00% respectively, for a composite of 2.20%.

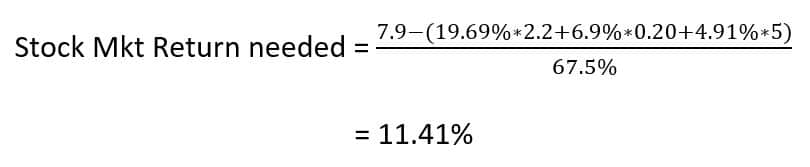

Remember that Risk Mitigation is just another synonym for Market Neutral hedge funds. I pulled a white paper on them from the web and it described the category’s ‘ambitious goal’ is for a return of 3% to 6% above that of Treasury bills. So let’s split the difference and say they earn 4.5% above the current rate for bills for a total return of 5%. Let’s lump in the real return category with equities. So now we can calculate the return the stocks need to get to earn the 7.9% return the fund is expecting. I’m just taking the equity percentage and dividing it by the weighted sum of the returns of the other categories.

What is a Realistic Return Assumption on New Jersey’s Assets?

That’s right. The politicians in New Jersey are assuming they can get a 11.4% return on their stock market holdings. That’s the only way to make the math work at today’s extremely low interest rates. How likely is this? It has almost a zero percent chance of happening. The historic 40 year old bull market saw the broad US stock market grow at an annual rate of 10%.

John Bogle recently reduced his 10 year stock market return prediction from 7% to 4%. He thinks the earnings multiple will decrease from an above average level of 20 to a long term average of 15. Let’s assume for a moment his new very reasonable forecast is wrong. For the pension fund’s sake, let’s stick with his original 7% expectation for stock market returns over the next 10 years. Using this number, let’s come up with an honest prediction for what New Jersey’s pension can earn in the next 10 years.

The Reason For This Assumption Is To Avoid Paying Billions of Dollars to Save the New Jersey Teachers’ Pension Fund

Just to be generous, let’s round up and say they get an even 5.5% each year over the next 10 years. That number is massively different from the 7.9% they are predicting. That 11.4% long term return on the stock market might have been achieved over one 10 year period in history. It’s virtually guaranteed never to repeat again, especially at today’s elevated valuation levels.

Why would New Jersey lie to the public and say they were going to get a return that’s impossible? It’s because it determines how much money they are obligated to contribute. If that 7.9% assumption were lowered, their minimum annual pension contribution would be billions of dollars higher. They lie through the accounting to get ratings agencies, investors, and teachers to think they will be able to pay pensions, when in fact they will have a gaping hole billions of dollars wide in less than 10 years.

Even At the Absurdly High Return Assumed by NJ, Their Contributions Are a Joke

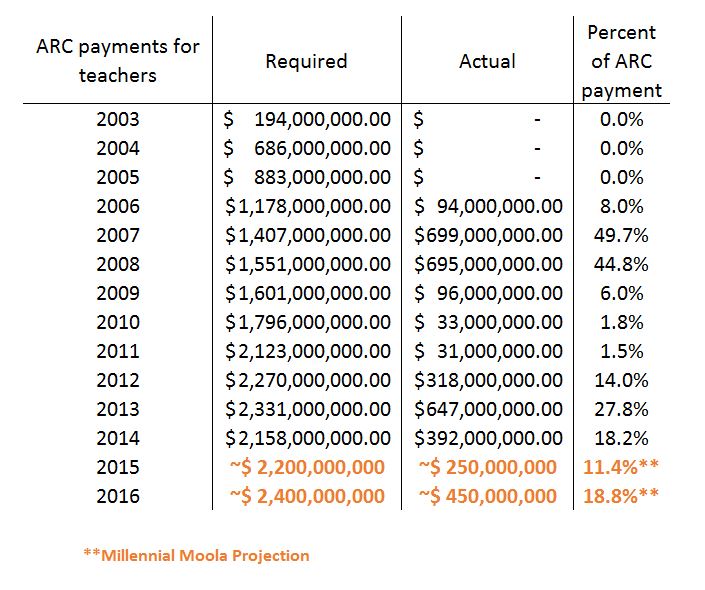

To see just how bad the situation is right now with the New Jersey Teachers’ Pension Fund, take a look at the contributions they’ve made since 2003. I pulled the data from the annual reports of the New Jersey Teachers’ Pension and Annuity Fund. Since 2014 is their latest annual report, I made assumptions as to what New Jersey will contribute in 2015 and 2016 based on their current budget plans.

A quick definition: ARC stands for Annually Required Contribution. It’s the number that pension professionals tell the state that they need to contribute to get the New Jersey Teachers’ Pension Fund back to full health. Remember this number is based on the ridiculous investment return assumption of 7.9%, meaning the Required column should be billions more if my realistic 5.5% return assumption was used instead.

Irresponsibility Followed by reform

The state somehow decided it would be a good idea to take a holiday from contributing ANYTHING to the fund for three years. They started ramping up contributions in 2007 only to be devastated by the economic collapse of 2008, obliterating their plan of getting the pension fully funded.

Here’s where it gets interesting. Governor Chris Christie gets elected and tells New Jersey teachers he will get their pension back to full health. He agrees to landmark legislation where teachers see their pension contributions rise from 5.5% to 7.5% of their paychecks over seven years. In exchange, he promised that the State would put in all of the money it had been withholding in years past.

chris christie pulls a fast one on the teachers’ union

The problem is that Chris Christie lied and didn’t keep his word. The state had some budget difficulties stemming from an $800 million surprise tax shortfall. He decided to balance the budget by not making the pension contribution the law he signed required. The teachers’ union sued him and lost. The court ruled that Christie was not obligated to make the contribution that his law required. The court justified their ruling on the principle that ‘one New Jersey legislature cannot bind another into debt.’

However, the court found that the promises to New Jersey workers must be kept. That means the state is still on the hook for the pension payments. However, it doesn’t have to contribute what it needs to for the fund to stay funded. All the court did was take the ticking pension bomb, make it vastly more destructive, and move it to the future.

Is the New Jersey Teachers’ Pension Fund Overly Generous?

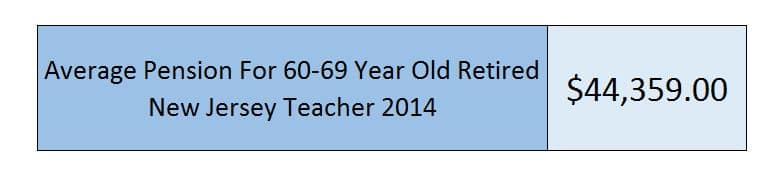

Many conservative politicians like to lament the huge giveaways to public sector unions, lambasting the pension payments as ridiculously large. While that might be the case in isolated incidents, the average retired NJ teacher does not make that much money from the pension. I dug into the annual report for 2014 and calculated the figure myself.

Clearly, this figure is not that high at all. Granted, it’s much higher than the average Social Security check, but it’s roughly one half to two thirds of the average annual salary of a teacher. I have a retired Florida teacher in my family. His pension is about two thirds of that amount, but New Jersey is way more expensive than Florida. The property taxes on a middle income house in New Jersey alone are enough to negate the benefits of the higher NJ pension.

contribution rates over time have increased for new jersey teachers

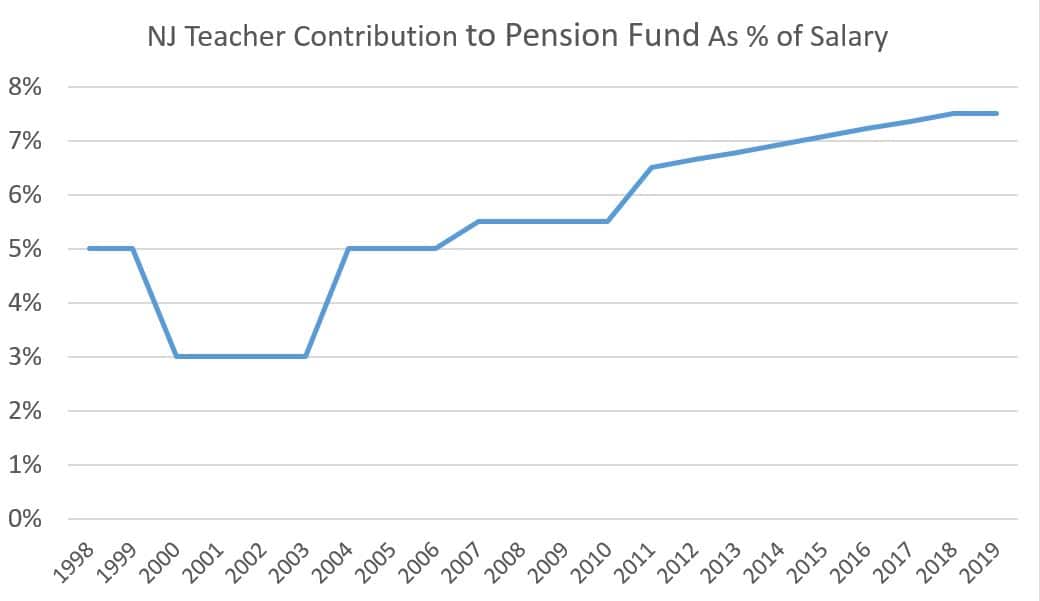

To see if the pension is too generous compared to a 401k style plan, let’s look at the contribution levels of NJ teachers over time.

In 2000, New Jersey was flush with pension cash. The stock market was at record highs. In fact, we were in the middle of the tech bubble, but state legislators didn’t know that. They reduced teachers’ contributions from 5% of salary to 3%. It took them a full four years to realize their mistake and move it back to 5%. The state gradually moved the level to 5.5%. In 2010, Christie finally worked with the legislature to pass a pension reform law. The legislation moved the teacher contribution rate to 7.5%.

Unfortunately, Christie did not live up to his end of the bargain. Even so, the teachers must all contribute the level specified in the law. So New Jersey teachers are fulfilling their part right? Even though they did exactly as asked of them, their current pension at the new 7.5% contribution level is still an incredible deal.

401k Versus State Pension Simulation: Which is Better For Current and Retired Teachers?

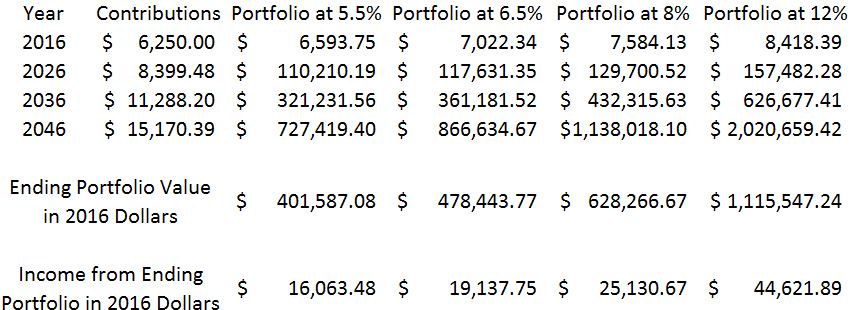

Assume that a New Jersey teacher joins the system as a young twenty something and used a 401k style plan instead with matching contributions. The private sector often contributes 4%, but since this is the public sector, let’s say the State contributed 5%. I assume the beginning salary is $50,000 with a first year contribution of $6,250.

I assume further that this contribution grows at a rate of 3% annually and inflation of 2% annually. In the columns below, I show different portfolio amounts based on different rates of return that the retiree could experience. In my analysis, I assume New Jersey earns a more realistic 5.5% return on their fund. I derive the income figure from the 4% rule, where you take 4% of the portfolio value and that figure and that money lasts for your entire retirement period.

Using the realistic 5.5% return, a retired teacher would end up with income of about a third of the average pension in 2014. She would need a 12% return just to get to the level of income that 60 something NJ retired educators are currently enjoying.

the verdict: the pension is more generous than even a fantastic 401k plan

So is the New Jersey teachers’ pension a good deal, even at the new 7.5% employee contribution minimum? It is an exceptionally good deal, as seen by the unrealistic 12% return needed to generate the average pension income. Since the S&P 500 index returned 10% annually over the past 40-50 years, teachers earning 12% a year after fees is unlikely.

However, that doesn’t change the fact that $44,000 is not a lot of money. Imagine you are a one income household and own your own home. Your adult children live in New Jersey and you hope to stay, despite sky high property taxes and cost of living. With that pension plus Social Security, you will probably have a comfortable retirement. However, if the state drastically reduced your pension, your retirement would surely take a turn for the worst. Perhaps some folks would need to return to work, downsize their homes, or move to a lower cost area away from friends and family.

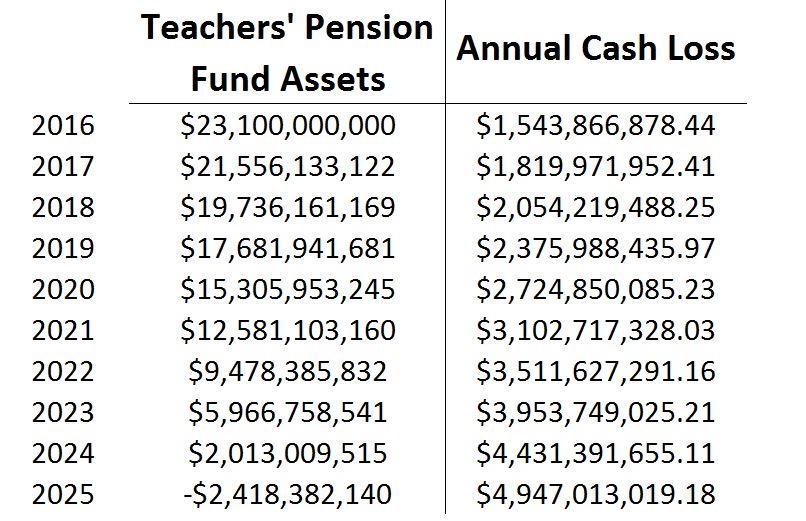

The Cold Hard Truth: The Math Behind the Claim

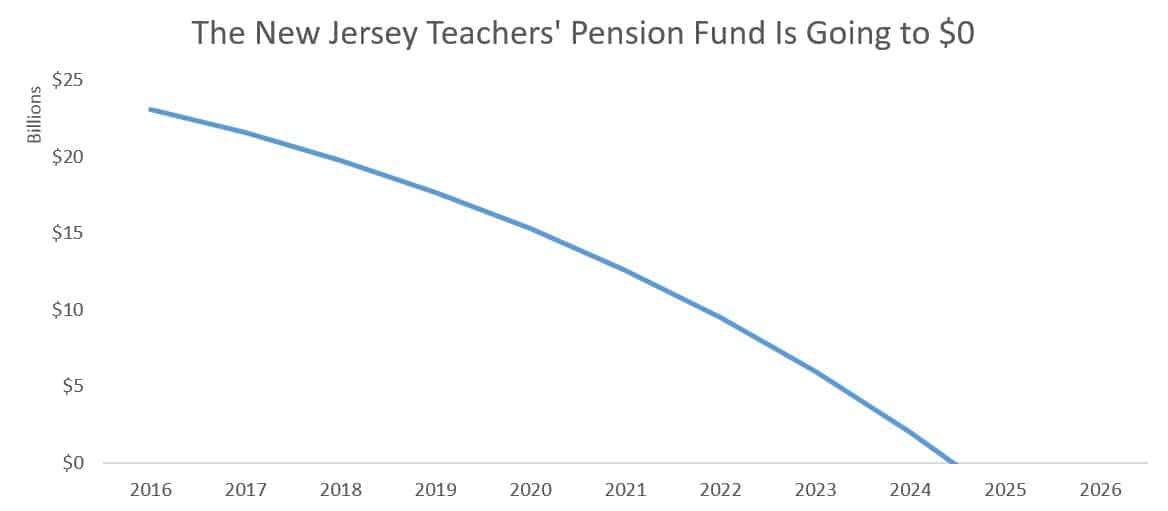

Check out the graphical representation of the decline in the New Jersey Teachers’ Pension Fund below. The fund starts off at $23.1 billion, my best guess as to what the assets are currently worth after this stock market plunge.

The 2014 benefit payment to all retired teachers was $3.89 billion. This payment level increased at approximately 4.5% since Christie enacted pension reform. Keep in mind this reform supposedly limited expensive pension features such as cost of living increases. I think that 4.5% rate of increase is likely to continue. There are almost 8,000 more active teachers in New Jersey over the age of 60 than there were in 2002 when this crisis started to develop (I figured that out from looking at every annual report for the New Jersey Teachers’ Pension Fund from 2002 to 2014). In fact, 4.5% benefit growth could be lowballing it severely. Even so, I want to be conservative in all my numbers to prove the point.

spending down pension fund capital causes a death spiral

New Jersey’s contribution in 2014 was low because of a revenue shortfall. The 2015 contribution was similarly low. Although, in 2016, the state increases it to $1.3 billion across all the state’s pension funds. I assume the New Jersey Teachers’ Pension Fund gets about a third of that as it’s about one third of the total assets. I use the 5.5% investment return assumption from earlier. After 2016, I increase the total net contribution to $1.5 billion and keep it at that level for the duration of the simulation. That is notably higher than the $1.184 billion in 2014, but again I’m being conservative. When you net everything out, the New Jersey Teachers’ Pension Fund burns through about $1.54 billion in 2016.

The losses accelerate because each year there’s a smaller pension fund generating less investment income. The fund managers handle the deficit by withdrawing more assets from the fund, which causes it to be even smaller. The investment income then shrinks for the following year. It’s a vicious cycle. Here’s the New Jersey Teachers’ Pension Fund size relative to the predicted deficit, which comes out of the fund’s assets.

New Jersey taxes are already sky high, with a risk of unexpectedly low tax receipts

Sometime between 2024 and 2025, the fund runs out of money. A New Jersey court has already ruled that the state must pay promised benefits. However, the state does not need to meet the minimum contributions to keep the pension funded. That means the fund will be out of money and New Jersey will have a $5 billion benefit payment to make in 2025. As a point of reference, New Jersey’s current 2016 state budget is around $33.8 billion.

Even though the budget is large, New Jersey currently has some of the highest taxes in the nation. The state economy could probably not survive drastic tax increases to pay for a $5 billion budget shortfall. Hence, the only solution would be enormous pension cuts and tax increases. After all, $5 billion is a huge number.

Are my assumptions and projections are too pessimistic? Consider that I made no predictions that New Jersey would have any more revenue surprises or other economic problems. New Jersey is currently running behind its projections on tax collections. New Jersey also collects a majority of its income tax revenue from the 10% richest residents of the state. These folks have a lot of income, especially from capital gains. Guess what type of income is likely to be way down in a stock market collapse? Capital gains.

I would worry right now if I predicted New Jersey state revenues that my previous estimates could be way off. Rich tax payers will have so many losses to claim on their taxes in 2015 and 2016 that tax receipts could fall. I have excluded any of these more pessimistic but possible situations. I want to keep all of my analysis very conservative in nature to show the magnitude of the pension crisis.

What I would do as a teacher or taxpayer in new jersey

If I was a teacher in New Jersey, I would be calling my elected officials every day. I would ask them what they are going to do to fix this crisis. I would be organizing my friends and coworkers to put the pressure on them. I would ask family, friends, loved ones, and even strangers to call and demand a solution before this crisis results in New Jersey’s bankruptcy.

If I was a New Jersey tax payer without any interest in protecting the benefits of teachers, I would be calling those same elected officials. I would demand benefit cuts for current and future New Jersey teachers to avoid draconian tax increases. Perhaps in exchange the teachers could go back to contributing 5.5% of their pay rather than 7.5%. I would also demand that a 401k style retirement plan replace the pension that is currently in place. That way, actuaries can define the massive unfunded benefit promises of today and the state can pay them down.

If You Know Any New Jersey Teachers, Warn Them

Instead, the Democratic legislature is blaming Chris Christie, who is blaming the Democratic legislature. While this crisis is spiraling out of control, what is Christie doing? Running for President. He’s using the vast underfunding of the pension to balance the budget. Unfortunately, Christie wants to look like he’s fiscally responsible and a good manager by kicking the can down the road. The truth is, he’s irresponsible at best and criminal at worst. His administration hides the ticking time bomb with ridiculously high investment assumptions and pension accounting. His pension payments to the fund continue to be tiny, and the New Jersey Teachers’ Pension Fund continues to spiral to $0.

If you know any educators in New Jersey, please warn them. They should not plan for the sunny retirement picture they hoped for. They will be facing down massive pension cuts, if they receive a pension check at all. If they plan on retiring, they need to start aggressively saving on their own in places like Individual Retirement Accounts. Both the recent stock market slump and recurring annual cash deficit assure that the value of the New Jersey Teachers’ Pension Fund will be $0 in less than 10 years.

*I will be adding updates as I find them in the comments section below.

What is your solution? Do you agree with this analysis? Would you want teachers to accept large benefit cuts or do you think politicians should raise taxes? Why do you think the media is not reporting the depth of this crisis in the midst of Christie’s presidential campaign? Comment below!

Update on 3/14/16: I’m still waiting to see the Director’s monthly investment reports to see how bad their January was. The S&P 500 was down about 5% for that month. Because the fund’s growth holdings are more aggressive, I expect it will down more than that. You can find these monthly reports here (note they usually come out about 1.5 to 2 months after the end of the month). http://www.nj.gov/treasury/doinvest/directorsreports.shtml

The comprehensive audited financials came out recently covering the period up until the end of June 2015. That can be found here: http://www.state.nj.us/treasury/pensions/pdf/financial/2015divisioncombined.pdf

The new balance of the New Jersey Teachers’ Pension Fund as of the end of that period has fallen to $25.6 billion, down from $27.2 billion. That’s down over 6%. The fund earned over $1 billion of investment income, or a 3.7% return before accounting for withdrawals. That means the funds own extremely optimistic 7.9% return will fail to cover the actuarial liabilities. In other words, the funds’ assets shrunk 6% in a positive year for investing. In a negative year, the compound effect of investment losses along with pension payments will remove the blinders from everyone’s eyes.

Another note is that the benefits spending continues to increase. In fiscal 2014, the total expenditure on benefits by the fund was $3.837 billion. In fiscal 2015, this spending grew 4.6% to $4.015 billion. Pension assets fell, spending went up, investment returns were positive, and still New Jersey’s bonds are trading well above 100 cents on the dollar. The market is irrational. If you’re a teacher in New Jersey or an investor in New Jersey bonds I would not expect to get the money that I was promised.

One last update for March. I ran a compounded rate of return for the S&P 500 from July 1, 2015 to February 29, 2016 and got -6.33%. That is probably a reasonable approximation of the return of the TPAF (Teachers’ Pension and Annuity Fund) through this period. If you just add the 6.15% drop in assets, subtract the investment return of 3.7%, and add the 6.33% drop in investments that I assume so far in this fiscal year, you get a 16.2% negative return on the $25.6 billion reported in June 2015. That would put the TPAF assets currently at only $21.45 billion, at the level I projected at the end of fiscal 2017. For this reason, the TPAF could run out even faster than mid-2024.

The state should offer lesser health plans to each employee along with the Cadillac plan. I believe many folks would choose it and would save some money. I can’t see why the unions would sue for giving folks a choice. Any savings need to go directly into the funds.

Your solution seems to be that the pensions will be cut drastically. Seems unfair since much of what the folks contributed went to help balance the budget. So they paid taxes twice and now you think the solution is they should/will lose their pensions. Come on now….

The solution should not just be one solution (teachers pension cut). The solution should be a combination of many things. Raise taxes by a bit, raise contributions by a bit, cut pensions by a bit, cut gov’t by a bit, offer lesser healthplans, etc. All those bits add up.

Also you say the plan is generous. I disagree. My husband and I started our careers back in the 70’s. I left teaching while making 14k. I immediately started making 19k and within one year was making 29k WITH BOTH A FREE PENSION (no contribution from me) AND a 66.66% match on a 401k!! Plus tons of other benefits. My husband stayed a teacher at a much lower pay then me. Seems to me he lost a lot of salary so the pension makes up for it!

Also not sure you take into consideration that the money at 2016 levels will also be getting interest while paying out. Also if anything is left in the 401k when that person dies, they get to leave that 401k to their kids. Not so with a teachers pension once they and spouse die. There are pros and cons to each. Did you know if the teacher dies before they retire, their spouse gets a pittance? So all that money they contributed…. If you are going to compare, please be honest and compare everything!

I read that by replacing the high level, high price health care plan with the next level down (still a good plan for teachers and retired teachers), it would save $2 billion dollars each year. If you put that $2 billion plus $1.5 billion from the state budget, would that not save the pension?

Considering that there are two other large pensions, the police/fire and the public employees, the $2 billion from healthcare savings wouldn’t be enough. It’s at 25% funded using a realistic investment return assumption. Plus the healthcare downgrade is Cadillac to bronze plan on Obamacare exchange I believe. Unions would rather sue first and see what happens

These government protected unions reap what they sow. 60-70k per yr for a teacher salary is ridiculous. And don’t cry me a river about the high taxes, it is the high government salaries and benefits that cause the high taxes….ever hear of cause and effect?

The unions might have a strong negotiating position since they hold a contract promising they’ll be paid no matter what. The only thing that might prevent them being made whole is a bankruptcy filing by the state

Regarding a bankruptcy by the state. States cannot go bankrupt. If they change the laws and allow them to go bankrupt, no one would want to lend to them. It would cause NJ more issues. They need to figure this out with a combination of:

1. Freeze their pensions. Pay what they have earned but going forward change the formula back to (avg of last 3 salaries x number of years / 65) instead of (avg of last 3 salaries x number of years / 55) for all workers. Keep their contributions at 7.5% or whatever they are now. In addition, only years of full time work should count. None of this 30 yrs of part time work, then the last 3 years of full time work at a huge salary to get a pension they didn’t pay for.

2. Find waste in gov’t and add it to the pension. I’m sure it’s there. Move the management of the pension back to non-hedge fund friends of Chris Christie. It costs 3 times to manage under Christie than in the past without the big returns they promised.

3. Offer the Cadillac healthplan they currently have, but the unions should not barf at offering them different plans such as a High Deductible plan which would be a huge savings to both the employee and the state. This plan is just as good, but really better. It makes the employee “shop” for the best price/care and not waste money. In the long run, healthy employees/famlies save huge amounts of money (and the state too), and sick families also save since there is a max out of pocket. Put any savings into the pension. Must be law that they must put it into and can’t touch it. That is key.

4. If the top 3 are not enough, raise taxes (shared sacrifice) by 1% and contributions by 1%.

BUT they should not go back on promises made. The pensions may seem like a great deal, you have to remember teachers who started in the 80’s made a lot less than the private sector over the last 40 years. And that money NOT made in the early part of their careers didn’t have a chance to grow. Also, after 40 years of teaching, if a teacher passes before they start their pension, they loose it and only get a small amount of money via insurance. Also as a spouse to a teacher, we’ve been paying $500 a month for an insurance policy to insure his pension in case he left me with 2 kids and years of payments into the system with no return.

Good points, I think health plan reform has the best opportunity to result in extra cash flow to the pension. The amount of waste in NJ isn’t as high as people think if you believe in social programs bc they have more assistance than red states in the south. If you look at the present value of the pension as promised today and include that in teachers’ salaries, they make about double the pay of the private sector. To only compare salary isn’t looking at the full picture. I’m sorry about that insurance policy that bites. I have lots of sympathy for teachers as my dad is a retired teacher. I just don’t know if the money’s there to leave things unchanged. They already raised the gas tax to one of the highest in the country, and it’s still not going to be enough. Any more increase in taxes and people will start leaving the state.

Really? 60-70k a year is too high?

What planet do you live on?

Teachers have gone to college and have masters degrees as well. You think you’d have anyone willing to do that job for less? You are simply crazy. I speak from experience. I used to be a teacher. I am now a programmer making well over 100k and my job is wayyyyy less demanding and wayyyy less hours than a teacher!!

Why is 60 K too high to educate a child? Do you have any idea what it’s like to teach 25 1st. grade kids how to read ? How about getting a class of 27 middle school students prepared for standardized math tests? Have you ever spent any time in a classroom since you were in school? Do you have any idea what a teacher deals with on an every day basis? What should a teacher make in your opinion, minimum wage? I could probably justify a pay cut for you as well.

I know what you are going to say, yes we are funded by taxes just as the cops, firefighters, sanitation workers, etc. It may come as a surprise to you but I also pay high taxes as do you. If 60 K is so high and appealing why not do as I did, put yourself in college debt and spend 4 years in school pursuing a noble profession that benefits society as a whole. Oh and while you’re at it, go visit your elementary school and if your overpaid teachers are still there sucking all your hard earned taxes from your paycheck, thank them for giving you the ability to construct a concise, well written blog.

wonderful article . I have recently left New Jersey after 13 years and have shared a similar perspective with the those I have left behind. I will share this with those folks.

Thank you James please do. The recent massive increase in the gasoline tax might put back my projections above by a year or two, but the broad premise is still accurate

I hope you will update this forecast once a clearer picture emerges of the coming federal political regime’s policies’ impact on the NJ’s Teachers’ Pension Fund. I may have to start planning some way to pay — no later than in my early thirties — for the retirement and medical bills of my mother, who has been serving as a public kindergarten teacher for over 35 years and has an extremely precarious heart condition. It’s a sickening and tragic state of affairs.

I definitely will update it in the months ahead. I want to wait to see what the new regimes policies will look like first. In short, federal bailouts for state teachers pension funds are now off the table so I definitely expect a more dire outcome for plan participants

It’ll be interesting to see how the governor’s race plays out with regards to the pensions. Seems like both candidates so far aren’t interested in talking about it.

Why would somebody talk about it right? That would require enormously painful decisions that can just be swept under the rug until the next governor comes into office. Look at Illinois right now and how they have a 9 month wait on bills that are supposed to be paid. That’s the future in NJ and it’s coming fast

Yeah pretty much. Kicking the can seems to be the tried and true strategy for dealing with this.

Any plans for an update or another article on NJ pensions or pensions in general?

I have no sympathy for the prospect of the pension fund being depleted. Most retired teachers don’t even realize that the entire amount of their salary that they have contributed toward their pension is returned to them within 3 years of being retired, and that doesn’t even consider the value of their Cadillac health insurance plans.

They will tell you that they paid into their pension and are therefore entitled to it, but they never do the math, because it doesn’t support their argument.

As a self-employed, single homeowner in New Jersey, the exhorbitant cost of property taxes and health insurance forced me to move out if the state – and I blame the overly generous salaries and pension plans of teachers and all state employees. Period.

How many teachers move out of the state after retiring and cease to contribute to the fund (via property taxes) that partially funds their pension? At the very least, pensions to retirees that move out of the state should be cut by 50%.

I’ve been self-employed for most of my life, making a salary similar to that of a NJ public school teacher (but working 12 months per year instead of 10), while also paying for my own health insurance, and will not even come close to being able to withdraw $44K per year from my self funded retirement account. I also have to settle for a bronze level garbage health insurance plan with a $6500 deductible because it’s all that I can afford.

They don’t even know how spoiled thay are, and that is, perhaps, the saddest part of all of this. They feel entitled due to their “service.” They have no sympathy for someone like myself who had to move out of New Jersey because of the high property taxes caused by them and their unions.

I have no sympathy for them. They’ve had it too good for too long and at the expense of others.

I hear the frustration on the taxpayer side. I too am stuck on a horrible bronze health care plan. I think what you’ll see in New Jersey is a continued push to squeeze every last dollar of revenue out of the residents of the state until people really start leaving in droves, at which point they’ll be forced to work out a settlement with pensioners or bankrupt their appropriation bondholders, which actually is a possibility unlike with general GO bonds.

Everyone thinks taxes are high because of pensions.

Well really?

They even thought they were high while the state was contributing NOTHING! So why were they high?

Yeah keep blaming teachers.

You got it! The bond holders will lose first and most!

“Most retired teachers don’t even realize that the entire amount of their salary that they have contributed toward their pension is returned to them within 3 years of being retired”

Do the math! 40 years of interest belongs to them as well, not the state (aka YOU). I sure don’t put my money somewhere without it gaining interest! Would you?

Teachers may only have to be IN the classroom for 10 months out of the year, but believe me all the weekends and nights more than make up for it! I work less hours in the private sector than my husband who is a teacher.

The people you should blame are the politicians. The costs for road repairs, and everything else if exhorbitant because of who they are paying off or hiring (their friends). Also the double dippers (again politicians), etc.

They brainwashed you into thinking it is the lower paid teachers and pw’s that caused this mess!

Not sure what you do for a living (folks never seem to post that!). Did you go to college? Do you need to take classes every year to keep your job?

And remember, teachers are tax payers too!

My husbands health insurance costs are 11k a year so stfu! You don’t know what you are talking about! He could have 43 years ago left teaching and gotten a much better paying job with better benefits. But NO he stayed and TAUGHT your kids and now you want to take more away from him now!

Annualizing the interest over 40 years on the contributions at a 10% rate of return would not even cover the cost of the pension that’s provided. I’m not saying that teachers aren’t deserving, my dad was a teacher after all and frequently took work home with him. Rather, the benefits for the entire state of NJ are out of control and will bankrupt the state. The teachers’ pension is the one in the worst shape which is why I profiled it.

In a state that has the highest property taxes in the country, has very high state income taxes and just lost its richest resident to Florida bc of those rates, and just hiked its gas tax to sky high levels, there aren’t any taxes to raise. The only way to save the state from bankruptcy in my view is aggressive cutting of benefits either for future retirees or kicking the can down the road where current retirees get hurt too. I truly feel for the teachers as they didn’t deserve this happening to them.

Have you ever seen how much a school administrator makes? Try 140K. And there are way too many of them! Governors admin worker make that much too.

But let’s pick on teachers because they make too much! LMAO!

I did a similar analysis earlier this year and have started to get ready ro get out of the state within the next two years. I see it as an excess financial risk to stay. Especially since no one has ever seen a state get to this point. Current law simply is unprepared to address what will happen and there is little chance of Federal help especially with other states (especially Illinois) in similar jeopardy.

Sounds like a smart move to me. The reflex reaction is going to be more taxes when the pension starts failing, so I’d certainly not own any huge property assets in New Jersey if it was me

I was wondering… as a teacher in the system now for about 14 years and paying into my medical insurance and not earning more then a 1% raise for the past 7 years… and seeing my take home salary go down year after year. Where is the money going that I pay into my insurance? I have not seen taxes go down or the money going into the pension and I know that the school board doesn’t use towards paying my insurance. Couldn’t that money go into paying the pensions?

Great point Laura but the cost of health insurance has soared like 100% or more since you started your job. It’s all going into the relentlessly rising cost of healthcare.

I started working June 1974 for a Fortune 500 company. After ten years I vested in the pension plan. Dec 1984 our CEO told us he was eliminating the pension plan and moving everyone to a 401k. Because of how the pension plan was made (hockey stick contributions) my lump sum payout was under $100. The same year we went the HMO route with a $500 deductible. He was up front and said “some of you might choose to work for another company, but these changes were a market shift that would impact most companies. These changes were made 33 years ago.

Over my 40 plus career I have worked for four Fortune 500 companies. All moved out of NJ due to high costs. Now 63, I am unemployed as my last employer moved out of state.

All state employees should be treated no better or worse than the typical taxpayer. Everyone on a 401k and paying at least 20% of their health ins cost. Perhaps salaries will need to be adjusted but we need to level the playing field.

I don’t have an answer on how to fix the NJ pension dilemma, nor do I have an answer on how to fix the SS dilemma. We should not fix one without fixing the other.

I think the NJ mess will hit first. Time will tell.

Question. If state government is suppose to pay in 1.5 billion ( or whatever the number is), where would that money come from? If teachers pay 7.5% of there salary towards the fund, where is the other money coming from. Not sure I am asking correctly but I can’t seem to wrap my head around where it is being pulled from the lottery, sales tax, gas tax , etc.

Also, has the state ever borrowed money from the fund and not paid that back or is they just keep sorting what it takes to potentially balance it.

They are basically taxing and borrowing everywhere they can to plug the hole temporarily.

Any update on the current situation of the TPAF Milliennial Moola?

Well it looks better than it did bc since I wrote this markets have done very well. But I would still say that the eventual path is the same. It might have just added a few years to its life.